Can China’s $140 Billion Motor Insurance Market Handle Rising Losses?

China’s motor insurance market is on track to become one of the largest in the world, with annual premiums expected to reach around $140 billion this year. Strong vehicle sales, supportive government policies, and the rapid rise of new energy vehicles (NEVs) are all pushing the market forward.

But beneath that growth story lies a growing concern: profitability.

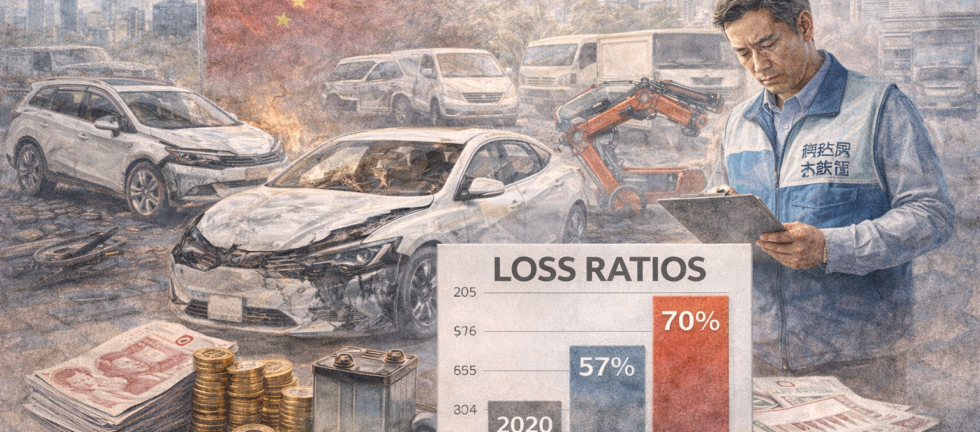

Over the past four years, loss ratios in China’s motor insurance sector have climbed sharply from about 57% in 2020 to roughly 70% in 2024. This means insurers are paying out far more in claims for every dollar they collect in premiums, raising questions about how sustainable the current model really is.

Growth Driven by Cars, Policy Changes, and Electric Vehicles

According to industry data, China’s motor insurance market is expected to continue expanding at an annual rate of just over 5% through 2030, potentially reaching $174 billion in gross written premiums.

Vehicle sales are a major driver. In 2024 alone, vehicle production increased by nearly 4%, while sales rose by about 4.5%. The momentum continued into 2025, with commercial vehicle sales and passenger car sales both posting double-digit growth during parts of the year.

Government incentives are also playing a big role. China’s vehicle trade-in program offers generous subsidies for consumers who scrap older cars and replace them with newer models especially electric vehicles. Buyers of new energy vehicles can receive higher subsidies than those purchasing traditional fuel-powered cars, along with purchase tax exemptions.

As a result, NEVs now make up nearly half of all new vehicle sales in China. Between January and July 2025 alone, NEV sales surged by more than 38% compared to the previous year.

Why Loss Ratios Are Rising

While the growth is impressive, it comes at a cost. NEVs are generally more expensive to insure than conventional vehicles. Repairs often involve costly batteries, specialized parts, and advanced technology that pushes up claim values.

Industry data shows that NEVs already account for around 15% of total motor insurance premiums, and their share continues to grow. As their numbers increase, insurers are facing higher repair bills, more complex claims, and greater exposure to loss severity.

This combination has pushed loss ratios steadily higher, creating pressure on underwriting margins.

How Insurers and Regulators Are Responding

To prevent affordability from becoming a major issue, regulators have stepped in with guidelines aimed at stabilizing the electric vehicle insurance market. Insurers, in turn, are adjusting their strategies.

Some companies are separating battery coverage from vehicle coverage. Others are introducing usage-based insurance and experimenting with telematics to better price risk. There is also a push toward risk-sharing arrangements for higher-risk vehicles.

At the same time, insurers are investing heavily in technology. Digital claims platforms, automated damage assessments, and improved customer service tools are being rolled out to control costs and improve efficiency.

Car manufacturers are also entering the insurance space, using their access to vehicle and battery data to design insurance products. In one notable move, regulators approved a major electric vehicle maker to offer compulsory motor liability insurance in selected regions.

The Road Ahead

Despite the challenges, the outlook for China’s motor insurance market remains broadly positive. Rising vehicle ownership, continued NEV adoption, and regulatory support are expected to keep premium growth steady over the next several years.

However, long-term success will depend on how well insurers adapt. Managing loss ratios will require better data, more refined pricing models, stronger claims automation, and closer cooperation with regulators and traffic authorities.

In short, China’s motor insurance market is growing fast but whether it can grow profitably will depend on how effectively insurers balance innovation, risk, and rising costs.

Source: Industry data and analysis based on GlobalData reporting